Roth accounts are among the most powerful tools in retirement planning. They offer tax-free growth, tax-free withdrawals, and no required minimum distributions (RMDs) during the account holder’s lifetime. However, income limits and contribution caps can restrict access, unless you know how to navigate the backdoor and mega backdoor Roth strategies.

The Strategic Value of Roth Accounts

Roth IRA Benefits:

- Tax-Free Growth: Investment gains grow tax-deferred and can be withdrawn tax-free in retirement.

- Tax-Free Withdrawals: Qualified distributions (after age 59½ and a 5-year holding period) are not subject to income tax.

- No RMDs: Unlike traditional IRAs, Roth IRAs are exempt from lifetime required minimum distributions.

- Estate Planning Advantage: Heirs receive tax-free distributions (subject to the 10-year rule if the assets are within the threshold)

2025 Contribution Limits:

- Contribution limit: $7,000 per year ($8,000 if age 50+)

- Income phase-out for Roth IRA eligibility:

- Single filers: Begins at $150,000, ends at $165,000

- Married filing jointly: Begins at $236,000, ends at $246,000

The Backdoor and the Mega Backdoor

Here is where the secret move comes in.

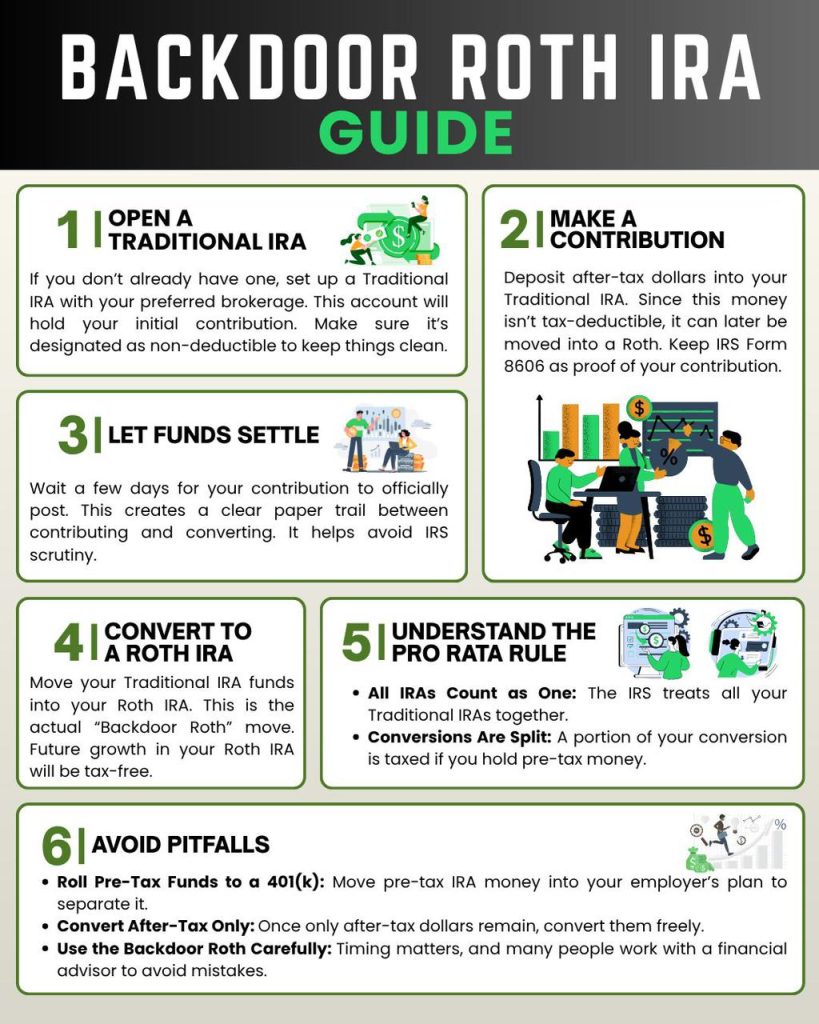

The Backdoor Roth

High-income earners who exceed Roth IRA contribution thresholds can still fund Roth accounts using a two-step process:

- Contribute to a Traditional IRA (non-deductible if income exceeds limits)

- Convert that amount to a Roth IRA—ideally soon after contribution to avoid taxable growth

Key Considerations

- Pro-Rata Rule: If you hold pre-tax IRA assets, the conversion may trigger partial taxation.

- Form 8606: Required to report non-deductible contributions and conversions.

- Timing: Best executed when pre-tax IRA balances are minimal or rolled into an employer plan (so only after-tax funds remain).

- Use Case: Ideal for high earners with limited access to direct Roth IRA contributions.

The Mega Backdoor Roth

The Mega Backdoor Roth allows significantly larger Roth contributions by leveraging after-tax contributions within a 401(k) plan.

Steps

- Make after-tax contributions to your 401(k) beyond the standard elective deferral limit.

- Convert those after-tax funds to Roth—either through an in-plan Roth conversion or rollover to a Roth IRA.

Requirements

Your employer plan must allow:

- After-tax (non-Roth) contributions

- In-service withdrawals or in-plan Roth conversions

2025 Limits:

- Employee elective deferral: $23,500

- Total 401(k) contribution limit (employee + employer + after-tax): $70,000 (or $76,500 if age 50+)

Strategic Benefits

- Supercharges Roth savings potential

- Creates tax-free retirement income

- Ideal for high earners with surplus cash flow

Why These Moves Matter

- Tax Diversification: Roth assets provide flexibility in managing taxable income during retirement

- Legislative Risk Mitigation: Roth accounts hedge against future tax rate increases

- Estate Efficiency: Roth IRAs pass to heirs income-tax free, preserving generational wealth if the assets are within the federal estate tax threshold.

These advanced moves allow individuals to bypass contribution limits and optimize long-term tax efficiency, especially when paired with other strategies like Roth conversions, asset location, and withdrawal sequencing.

The Next Chapter: 401k, IRA, and SEP IRA

Now that you’ve unlocked Roth strategies, it’s time to explore the foundational accounts that support them. Understanding how 401(k)s, IRAs, and SEP IRAs work will help you structure your retirement plan and integrate Roth strategies for maximum impact.

Stay tuned. This is where your financial playbook starts to get really exciting.