ILIT stands for Irrevocable Life Insurance Trust. It is a legal entity created for the purpose of owning a life insurance policy. The trust is considered “irrevocable” because once it is created, it cannot be modified or terminated by the grantor (the person who creates the trust).

The way an ILIT works is that the grantor transfers ownership of a life insurance policy to the trust, and then the trust becomes the owner of the policy. The grantor can name their desired beneficiaries in the trust document, and upon the grantor’s death, the death benefit from the policy is paid to the trust. The trust then distributes the death benefit to the beneficiaries according to the trust document.

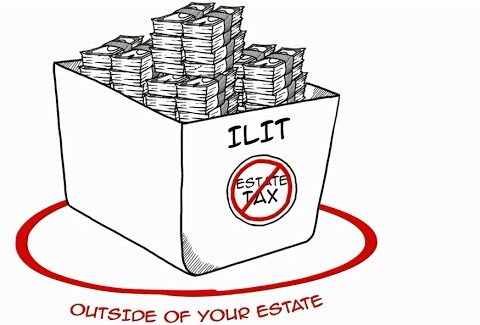

One of the main advantages of an ILIT is that the death benefit is not included in the grantor’s taxable estate, which can potentially save a significant amount in estate taxes. Additionally, the trust can provide some level of creditor protection for the beneficiaries, as the death benefit is not considered part of their personal assets.

However, there are some potential downsides to creating an ILIT, including the loss of control over the life insurance policy and the requirement for the trust to have its own tax identification number and file its own tax returns. It is important to consult with a qualified financial advisor or attorney to determine if an ILIT is appropriate for your individual situation.

Steps involved in creating ILIT:

- Create an irrevocable trust – This involves working with an attorney to create the trust document that specifies the trust’s beneficiaries and trustee, the terms of the trust, and the conditions for distributing assets.

- Transfer life insurance policy ownership to the trust – The grantor must transfer ownership of the life insurance policy to the trust, which requires completing and signing an ownership transfer form.

- Pay insurance premiums – The trustee pays the premiums on the life insurance policy from the trust’s funds.

- Death of the grantor – When the grantor passes away, the death benefit from the life insurance policy is paid to the trust.

- Distribution to beneficiaries – The trustee distributes the death benefit according to the terms of the trust document, which specifies the beneficiaries and the distribution terms.

- Ongoing management – The trustee is responsible for managing the trust’s assets, which may include investing the funds, paying taxes, and filing tax returns for the trust.