The IRS used to use the Consumer Price Index (CPI) to calculate the past year’s inflation. However, with the Tax Cuts and Jobs Act of 2017, the IRS will now use the Chained Consumer Price Index (C-CPI) to adjust income thresholds, deduction amounts, and credit values accordingly.

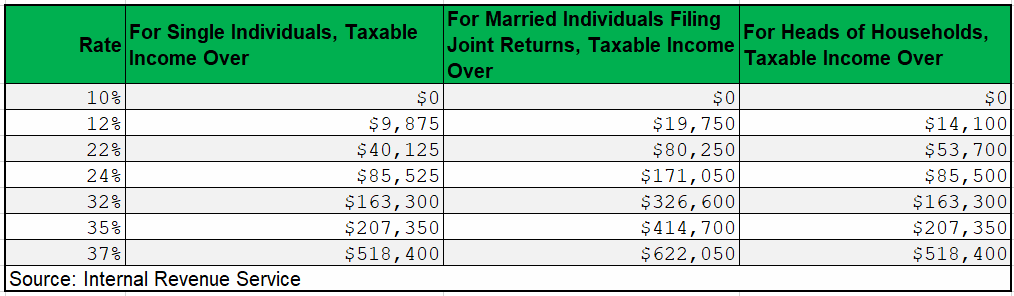

2020 Federal Income Tax Brackets and Rates

In 2020, the income limits for all tax brackets and all filers will be adjusted for inflation and will be as follows as shown below. The top marginal income tax rate of 37 percent will hit taxpayers with taxable income of $518,400 and higher for single filers and $622,050 and higher for married couples filing jointly.

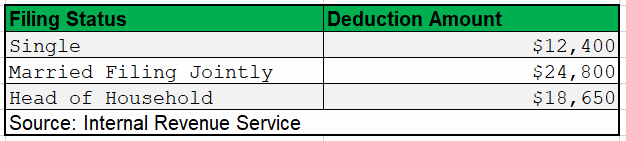

Standard Deduction and Personal Exemption

The standard deduction for single filers will increase by $200, and by $400 for married couples filing jointly. The personal exemption for 2020 remains eliminated.

Alternative Minimum Tax

The Alternative Minimum Tax (AMT) was created in the 1960s to prevent high-income taxpayers from avoiding the individual income tax. This parallel tax income system requires high-income taxpayers to calculate their tax bill twice: once under the ordinary income tax system and again under the AMT. The taxpayer then needs to pay the higher of the two.

The AMT uses an alternative definition of taxable income called Alternative Minimum Taxable Income (AMTI). To prevent low- and middle-income taxpayers from being subjected to the AMT, taxpayers are allowed to exempt a significant amount of their income from AMTI. However, this exemption phases out for high-income taxpayers. The AMT is levied at two rates: 26 percent and 28 percent.

The AMT exemption amount for 2020 is $72,900 for singles and $113,400 for married couples filing jointly.

In 2020, the 28 percent AMT rate applies to excess AMTI of $197,900 for all taxpayers ($98,950 for married couples filing separate returns).

AMT exemptions phase out at 25 cents per dollar earned once taxpayer AMTI hits a certain threshold. In 2020, the exemption will start phasing out at $518,400 in AMTI for single filers and $1,036,800 for married taxpayers filing jointly

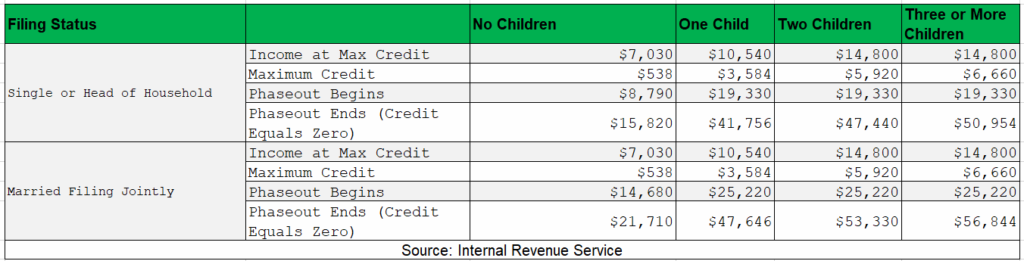

Earned Income Tax Credit

The maximum Earned Income Tax Credit in 2020 for single and joint filers is $538, if there are no children. The maximum credit is $3,584 for one child, $5,920 for two children, and $6,660 for three or more children. All these are relatively small increases from 2019.

Child Tax Credit

The child tax credit totals at $2,000 per qualifying child and is not adjusted for inflation. However, the refundable portion of the Child Tax Credit is adjusted for inflation but will remain at $1,400 for 2020.

Capital Gains

Long-term capital gains are taxed using different brackets and rates than ordinary income.

Qualified Business Income Deduction (Sec. 199A)

The Tax Cuts and Jobs Act includes a 20 percent deduction for pass-through businesses against up to $163,300 of qualified business income for single taxpayers and $326,600 for married taxpayers filing jointly.

Annual Exclusion for Gifts

In 2020, the first $15,000 of gifts to any person is excluded from tax. The exclusion is increased to $157,000 for gifts to spouses who are not citizens of the United States.

More information on 2020 Tax Rule https://taxfoundation.org/